For Week Ending November 19, 2022 (Data current as of Nov. 28, 2022)

Weekly market activity data and reports are provided by ShowingTime, and updated on Mondays by 2:00 pm, once received. Exceptions are on Monday holidays, when data/reports are not available until the following day.

Housing supply continues to grow nationwide, as higher borrowing costs cause home sales to slow. According to Realtor.com’s Monthly Housing Market Trends Report, the national inventory of active listings increased 33.5% year-over-year in October, the highest inventory level since 2020. As a result, local buyers may find they have more options to choose from, and with homes spending more days on market compared to the same period last year, a bit more time to shop around as well.

Charlotte Region

In the Charlotte region, for the week ending November 19:

New Listings decreased 34.5% to 759

Pending Sales decreased 34.2% to 747

Inventory increased 49.7% to 7,784

For the month of October:

Median Sales Price increased 13.4% to $380,000

List to Close increased 16.7% to 84

Percent of Original List Price Received decreased 4.0% to 96.5%

Months Supply of Homes for Sale increased 72.7% to 1.9

In today’s sellers’ market, many homeowners are weighing their options and trying to decide if they should sell their house. If you’re in that group, you may be balancing things like the ongoing health crisis, rising mortgage rates, and your own changing needs to determine your best time to make a move.

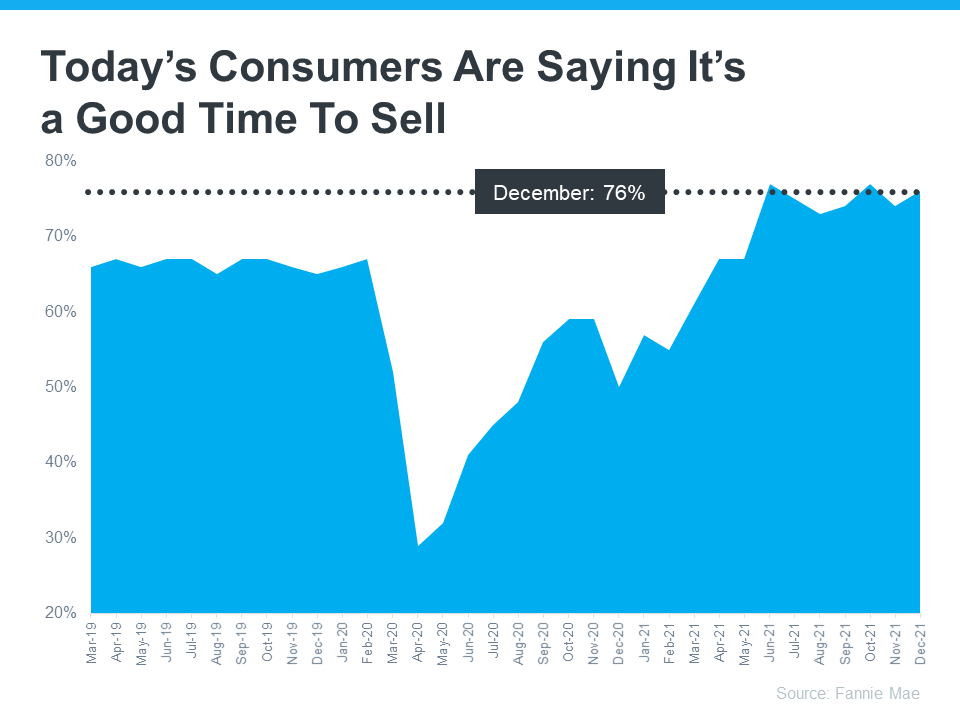

However, recent data shows that time may already be here. According to the latest Home Purchase Sentiment Index (HPSI) by Fannie Mae, 76% of consumers believe now is a good time to sell.

Looking back over the past few years, its clear consumers are incredibly optimistic today. The graph below shows the percent of survey respondents who say it’s a good time to sell a house, and their positive outlook is on the rise. The big dip near the middle of the chart indicates how consumer sentiment about selling dropped at the beginning of the pandemic as uncertainty about the health crisis and its impact grew. The good news is, the trend today shows a continued, drastic improvement, and people are feeling more and more confident with time about selling a home.

In fact, survey respondents think it’s an even better time to sell a house today than they did in the lead-up to the health crisis. The latest survey results indicate we’re at one of the strongest peaks in seller sentiment since March of 2019, hitting highs when 77% of people thought it was a good time to sell only twice before in June and October of 2021.

Why Are Consumers So Optimistic About Today’s Housing Market?

From record-high equity gains to record-low housing supply and significant buyer demand, homeowners have more motivation than ever to sell. There are more buyers in today’s market than there are homes for sale, and that’s driving home prices up, making it a great time to sell your house.

According to the National Association of Realtors (NAR), the current supply of homes for sale today is at a 1.8-month supply, which is an all-time low. When the supply of homes for sale is low, sellers will likely see more offers, which is exactly what’s happening right now. As NAR notes:

“The average home for sale is receiving 3.8 offers today, up from 3.3 offers just one year ago.”

Bottom Line

With the inventory of houses for sale so low today pushing home prices in an upward direction, it’s no wonder consumers think it’s a good time to sell. If you’re ready to take advantage of today’s favorable sellers’ market, let’s connect today.

You’re officially making the big move from one city to another. Maybe you’ve landed a new job or have decided you want to travel to a new city to explore and live a little. All your bags are packed, you’ve said goodbye to friends and family and you’re ready to hit the road to the new city you will soon call home. One of the biggest decisions you will come across is whether you should rent or buy. Here are a couple of reasons why renting is better than buying for the first couple of years living in a new city.

It takes time to learn a new city, new neighborhood, and possibly even a new culture. Within the first month, you may be completely in love with your new city. It’s easy to be blinded by the excitement of living in a new place because it’s all brand new to you. After living there a few months, things could change. You could end up hating the area that you are living in. If you were renting, it would be much easier to move to a different neighborhood than if you were tied into making monthly payments on a mortgage for a house.

A lot can change in a year. You could end up hating your new job and your new boss. What if your old boss wanted to hire you back? It would be easier to move back home for your old job if you were only renting a place for a year versus if you had purchased a home. If you had bought a house, you would most likely be coughing up your own money to pay off your mortgage and pay for closings costs because your home had not increased in value in such a short amount of time.

All in all, it’s best to give yourself a few years to really learn a new city, in every aspect, before making a long-term commitment, like purchasing a house. Give yourself time to explore the city and all that it has to offer. Maybe after your first year, you’ll find an even better neighborhood to live in that fit your needs perfectly.

According to Business Insider, Homebuilding giant PulteGroup reported Q3 net income of $117 million or $0.30 per share. This was a big improvement from last year’s $0.34 net loss.

According to Pulte CEO, Richard Dugas: “In past cycles, the U.S. housing industry proved to be a powerful engine that could help drive the economy forward and accelerate the pace of a recovery. A similar scenario could again be unfolding, as the industry is responding to increased sales by hiring additional workers and purchasing more building materials. While we are mindful of any potential impact from global or domestic economic issues,we are optimistic that the combination of ever higher rental rates, record low interest rates and limited housing supply can continue to support the improved housing demand.

In Charlotte, we have seen an increase in closing and a decrease in inventory pointing towards a very minor switch from a buyers market to a sellers market. However, we are very mindful of the still looming Charlotte Foreclosures and Lake Norman Foreclosures that still impacts the ‘everyday’ Charlotte area seller.

If you share our enthusiasm for honesty, integrity, and quality of service, we’d like to help market your services to homeowners in the Charlotte and Lake Norman areas. We need your business description, including details,website if any and testimonials. If accepted your contact information will be provided to all customers who search for your business category on our website.

Here are a few tests we require that to be on our list:

Pass reference checks and business license verification

Maintain general liability insurance

Earn satisfaction rating from our customers when we follow-up

Are you thinking of buying or selling in The Charlotte and Lake Norman Areas? Why not ask Carolina Living Real Estate about their services?

Not only do we use the latest technologies, we pay our agents 100% commission and just take a transaction fee.

What does this mean to the consumer (Homeowner)? Our agents are not giving a substantial amount to us (the Broker) allowing them to negotiate how they want to ‘get the deal done’!!

These savings can be used on both the seller and the buyer seller. There are a couple of legal ways to pass this savings on to YOU!.

All you need to do is call us (704 412 4009 or 704 451 7051) and ask how!

You see expired and withdrawn listings in the Charlotte area are not the product of smaller companies. They are a part of the business of selling real estate for all companies. However, with a firm like ours, the agents have SO many tools at their disposal, including negotiating with our own money. You see our agents keep the bulk of it and as we all know, Money is Power!

Let’s make 2012 the year Charlotte Real Estate bounces back…

Our new Offer To Purchase that was put in affect in January of 2011 has brought on some much needed fairness to the seller. The seller is paid a due diligence fee by the buyer to allow the buyer to investigate the property.

Really the most important aspect of buying a house is now in the preparation. It never should have been up to the seller to determine the buyer’s credit worthiness. Now that we have a due diligence period, the contract should only be about the property. After all it is an offer to purchase a property.

The buyer should investigate his/her credit worthiness and be comfortable with it before EVER writing a contract. You see the due diligence will only really work as intended if the buyer is pretty sure they can be approved for a loan.

So, what are the steps for loan approval?

Pre-Qualification

This occurs when the buyer provides information about income, assets and liabilities to a lender and allows a credit report to be run. Pre-Approval

This step requires confirmation of income and assets through thorough documentation like bank statements, paystubs, W2’s and tax returns. Final Approval

This occurs when all information is validated and an appraisal is completed that is acceptable to his/her lender.

So where should the buyer be before writing an offer? They should have completed the Pre-Approval process. This would only leave selecting the property and having the appraisal done along with other ‘property’ inspections. You see the due diligence should only include issues with the home and not issue with the buyers credit worthiness.

If the buyer is PREPARED, the due diligence period can be done in 10-15 days and the due diligence amount can be a small sum of money or ZERO!

I recently read a great article on Trulia.com by Tara-Nicholle Nelson. It speaks to the difficulties in buying and selling real estate with regard to the documentation you will need to actually buy or sell a home. Buyers and Sellers are both becoming very frustrated with the numerous requests made by lenders for more documentation. It is best to be prepared. Tara was kind enough to provide the following list and explanation.

ID (e.g., driver’s license, state-issued ID, passport). Who must produce it? Buyers and sellers. Why? Uh, hello!?! Lender wants to know that you are who you say you are, buyers, and the title insurance company wants to make sure, sellers, that you actually have the right to sell the home. Funny enough, this commonly goes unrequested until you get to the closing table, when the notary requests to see it before signing, but some mortgage brokers and even some real estate brokers and agents may ask to see it earlier on.

Paycheck Stubs. Who must produce it? Any buyer financing their purchase with a mortgage. Sellers, usually only in the case of a short sale. Why? Buyers’ purchase price ranges are determined, in part, by their income. And short sellers have to prove an economic hardship.

Two months’ bank account statements. Who must produce it? Buyers getting financing; sellers selling short. Why? Buyers’ lenders now require proof of regular income and proof that the down payment money is your own. Short sellers? It’s all about the hardship.

Two years’ W-2 forms or tax returns. Who must produce it? Mortgage-seeking buyers and short selling sellers. Why? Banks want to see a stable, long-term income. They also limit you to claiming as income the amount on which you pay taxes (attn: all business owners!). And in short sales, again, they want documentation of every single facet of your finances.

Updated everything. Who must produce it? Buyer/mortgage applicants. Why? Because things change, and because the time period between the first loan application and closing can be many months – even years! – on today’s market. During the time between contract and closing it’s not at all unusual for underwriters to demand buyers produce updated mortgage statements, checks stubs, and such – and its quite common for them to call your office the day before closing to request a last minute verification of employment!

Quitclaim deed. Who must produce it? Married buyers purchasing homes they plan to own as separate property. Married sellers selling homes that they own separately, or joint owners selling their interests separately. Why? With the Quitclaim Deed, the other spouse or owner signs any and all interests they even might have had in the property over the the selling owner, making it possible for the title insurer to guarantee clear, undisputed title is being transferred in the sale.

Divorce decree. Who must produce it? Buyers and sellers who need to document their solo status or the property-splitting terms of their divorce. Why? Again, to ensure that the seller has the right to sell. Recently single buyers might need to prove that they shouldn’t be held to account for their ex’s separate debts or credit report dings.

Gift letters. Who must produce it? Buyers using gift money toward their down payment. Why? The bank wants to be sure the gift came from a relative, and is their own money to give. They also want the relative to confirm in writing that it’s a gift, not a loan – a loan would need to be factored into your debt load.

Compliance certificates. Who must produce it? Usually sellers, but sometimes buyers, by contract. Why? Some local governments require various condition requirements be met before the property is transferred, like some cities which require a sewer line be video scoped and repaired, cities which require a checklist of items be met before a certificate of occupancy be issued (usually relevant to brand new and really old homes, the latter of which are often subject to lead paint concerns) and energy conservation ordinances which require low-flow toilets and shower heads to be installed. Ask your real estate pro for advice about which, if any, such ordinances apply in your area.

Mortgage statements. Who must produce it? Any seller with a mortgage. Why? the escrow holder or title company will need to use them to order payoff demands from any mortgage holder who has to get paid before the property’s title can be transferred.

Carolina Living Real Estate and Carolina Living Property Management serving the Charlotte and Lake Norman areas as well as points North, South, East and West has earned an A with the Better Business Bureau! Click on the picture to learn more about our services. We charge a very low 8% management fee with ZERO start up costs. Check out this great service! Visit the Carolina Living Property Management Website!